The San Francisco Bay Area is one of the best places in the world. There’s Silicon Valley, which is responsible for some of the most innovative and ground-breaking of our time. Plus, the Bay Area is home to a wide variety of cultures and urban settings. Nature, from luxuriant redwood woods to undulating, green hills, surrounds the entire area and is only a short distance from the beach. Indeed, the Bay Area is one of the best places to call home.

However, if you want to reside in the Bay Area, is it best to rent or buy a home? There are many advantages and disadvantages of renting, buying, and/or selling homes in the Bay Area, and this blog will try and point out a few of them.

Pros of Renting a Home in the Bay Area

1. Fewer Bills

If you rent a home, you have fewer bills to pay compared to homeownership because you don’t have to pay property taxes or any homeowner fees. Renting allows you to just pay your landlord, and they have to deal with all the taxes and fees.

2. Don’t Have To Worry About Maintenance

You won’t be responsible for maintenance or repairs. It is the responsibility of the landlord to take care of required maintenance, such as replacing the water heater or other home maintenance issues. It’s one great advantage that will save you time and money.

3. Flexible Situation

Renting a home in the Bay Area means that your home situation is flexible. If you’re a renter and you need to move homes, you can choose between not renewing or ending your lease early. You don’t have to worry about selling a home.

Cons of Renting a Home in the Bay Area

1. Expensive

Renting can be expensive in the Bay Area. To control inflation, the government has increased interest rates, which also affects rent. Rent in the Bay Area can be $5,000 a month or more. You may be able to find a place for less than $3000, but those are typically smaller units and not in the best and safest areas. If you stop renting or decide to terminate your lease, you don’t get anything back from your monthly payment. You’re essentially building home equity for your landlord.

2. Most Costly in the Long Term

Renting in the Bay Area will cost you more in the long run. House rentals have an average yearly rental increase of 6%. If you’re renting a home for $2,785 per month in your first year, you’ll be paying $3,516 per month in your 5th year. In just a short period, your monthly rent can drastically increase.

3. No Equity

Renting a house in the Bay Area prevents you from building equity. Even if you can call it your home, your rental isn’t an asset. Also, there is no tax benefit to renting.

Pros of Buying a Home in the Bay Area

1. Almost the Same Cost as Renting

In the Bay Area, home values in some areas have decreased by as much as 10% to 20%. As a result, purchasing now with an adjustable mortgage could result in lower annual and total tax payments. Additionally, if interest rates decline, the loan can be refinanced. For instance, the monthly payment for financing and purchasing a property in the Bay Area may be $3,490. However, you will own the house and receive tangible and intangible benefits from your monthly payment. If you had been renting, you would have been spending the same amount every month, and your landlord gets the increase in home equity and tax advantages.

2. A Good Course of Action During a Recession

Purchasing real estate can be a good hedge against inflation. As inflation climbs, the government will try to slow inflation by raising interest rates. Once inflation slows, the government will eventually lower interest rates. To put it another way, inflation affects mortgage rates. If you had purchased a home now at a high rate, you may be able to refinance at a reduced rate. In addition, buying a home in a buyer’s market can help avoid bidding wars. When interest rates start to fall, buyers who have been holding off will be back in the market. If there is still low housing availability, bidding wars and rising home prices may return.

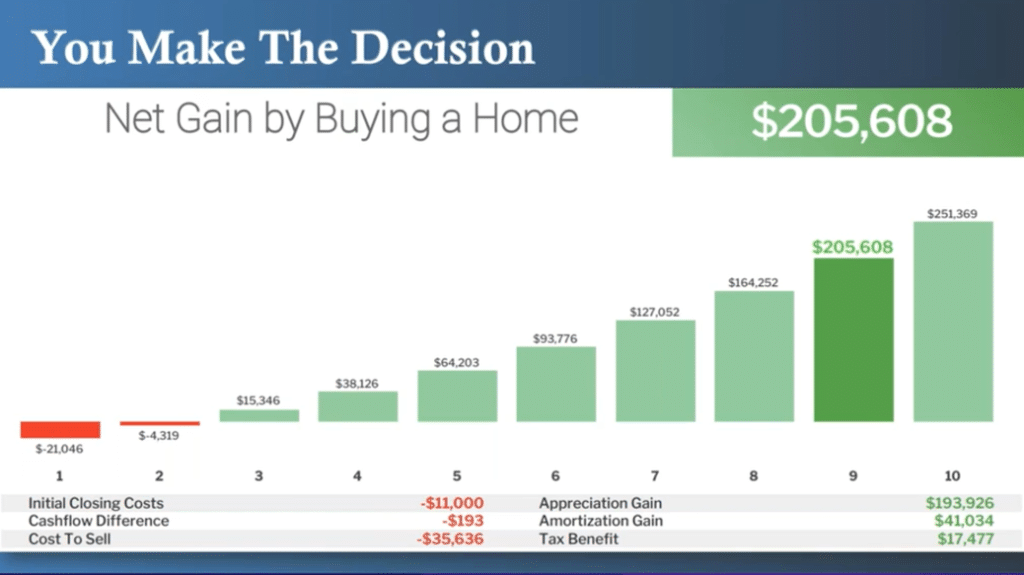

3. Build Equity

Buying a home in the Bay Area will allow you to build home equity. Owning a home is considered by many as an important part of building wealth. The average forecasted appreciation rate per year is 4.49%. For example, if you’re paying $3,490 per month for a $400,000 home, you could have a net gain of $205,608 after you fully pay off the home. In addition, you’ll get tax benefits along the way. Moreover, the net gain can increase if you refinance your home at a much lower interest rate along the way. (Example is for illustration purposes only).

Cons of Buying a Home in the Bay Area

1. Down Payment Costs

To buy a house, you’ll need to put down cash as a down payment. For example, a $40,000 10% down payment on a $400,000 home may be necessary to obtain a mortgage loan. A down payment of $40,000 can be difficult for some people.

2. Mortgage Payments

In comparison to renting, buying a house in the Bay Area may require higher monthly mortgage payments in the beginning. However, mortgage payments will probably be fixed through the life of a loan. And, due to the cost of selling a home, purchasing a home might not be for you if you don’t intend to live there for at least two years.

3. Less Flexibility

Buying a home can make it challenging to move or relocate for short-term residents of the Bay Area. Selling a home is more difficult than breaking a rental lease.

Bottom Line

Whether you should buy a home or rent one will mostly depend on your needs. If you won’t be living in the Bay Area for more than two years, renting is usually preferable. But if you plan to stay for more than two years, buying a house can be the best solution. It will require more money upfront, but in the long term, it can be worth it. Due to tax benefits, appreciation, and other intangible benefits, you will probably get more for your money.